Why you should switch to a Tax-Free 401k Alternative.

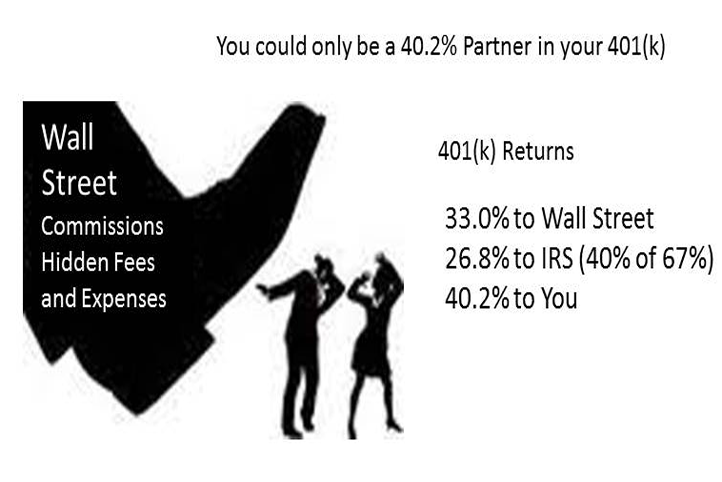

The Tax Free 401k Alternative eliminates 3 wealth killing elements of a 401k: Market losses, Taxes and Wall Street Commissions, Hidden Fees and ExpensesYou may only be a 40.2% Partner in your 401k. Wall Street and the IRS own the rest.

The Tax Free 401(k) alternative has been called the perfect retirement solution. It has been used by the wealthiest American Families for more than 20 years to cut taxes and preserve capital.

It eliminates the 3 Wealth Killers dragging down 401k returns: Market Losses, Taxes and Wall Street hidden fees, commissions and expenses.

The Tax Free 401k eliminates 3 wealth killers dragging down 401k returns.

It has been called the perfect solution because:

You don’t lose money when the markets go down, so you are never digging out of an investment hole.

You share in market upside when the markets go up, subject to an annual market cap rate, currently 13% to 16%.

You’ll earn a reasonable rate of return.

Gains are locked in annually, so you never give back profits previously earned.

Withdrawals are tax-free penalty free at any age for any reason.

Will you be strapped for cash in retirement or will your retirement dreams be restored? Will you enjoy travel, leisure activities like golf, quality time with your grand children, and activities with your spouse?

The Tax-Free 401k can help make your retirement years special, helping you accumulate enough money to provide income for 30 to 40 years of retirement.

The Tax-Free 401k Alternative eliminates 3 Wealth Killers:

Market losses

Taxes

Wall Street commissions, hidden fees and expenses.

Market losses are forever and compound just like gains. The money lost never works for you again. Remaining funds have to do double duty playing catch up as you dig out of an investment hole.

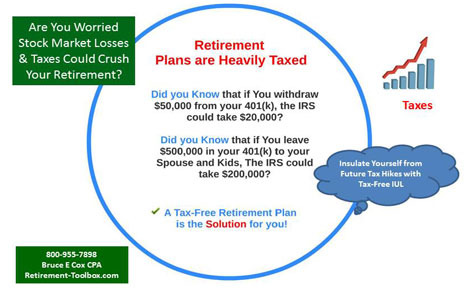

Taxes are another wealth killer. Did you know that if you withdraw $50,000 from your 401(K) the IRS could take $20,000? If you leave $500,000 to your spouse and kids in your 401(k) the IRS could take $200,000?

Your 401(k) is one of the most expensive ways to save for retirement. Wall Street Commissions, hidden fees and expenses can reduce your 401(k) balance by 33% over 30 years. In other words, after 30 years, your 401(k) balance would be 50% higher without these fees. This could cost you more than $500,000 over your working years.

Bottom line, you may only be a 40.2% partner in your 401(K)

33.0% to Wall Street

26.8 % to IRS (40% of 67%)

40.2% to you

Wall Street Commissions, Hidden Fees and Expenses could take a third of your retirement account over 30 years. Add in Taxes and you might only be a 40.2% Partner in your 401k.

The Perfect Retirement Solution, known as a Tax-Free Retirement Plan, a Tax-Free Pension Alternative, Living Benefit Life Insurance and a Tax-Free IUL eliminates the 3 Wealth Killers: Market losses, Taxes and Wall Street commissions, hidden fees and expenses.

The Tax-Free 401k Alternative eliminates 3 wealth killers dragging down 401k returns.

It has been called the perfect solution because:

You don’t lose money when the markets go down, so you are never digging out of an investment hole.

You share in market upside when the markets go up, subject to an annual market cap rate, currently 13% to 16%.

You’ll earn a reasonable rate of return.

Gains are locked in annually, so you never give back profits previously earned.

Withdrawals are tax-free penalty free at any age for any reason.

Tax-Free is better. Watch the short video and call us with comments and questions.

The Perfect Retirement Solution, also known as a Tax-Free Pension Alternative, Living Benefit Life Insurance and a Tax-Free IUL solves this wealth killer by eliminating taxes and penalties on withdrawals.

It has been called the perfect solution because:

You don’t lose money when the markets go down, so you are never digging out of an investment hole.

You share in market upside when the markets go up, subject to an annual market cap rate, currently 13% to 16%.

You’ll earn a reasonable rate of return.

Gains are locked in annually, so you never give back profits previously earned.

Withdrawals are tax-free penalty free at any age for any reason.

Are there better options available you are not aware of? Most likely the answer is yes. So, when do you want to find out, now when you can do something about it, or 20 years from now when it might be too late to shift course?

There has been a “Paradigm Shift” in Retirement Planning. New thinking could triple your income after-taxes compared to 401(k) or 403(b) plan income.

This favorable IRS allowed strategy lends itself to “Zero” Tolerance for Retirement Taxes and “Zero” Tolerance for Stock Market Losses.

You no longer have to risk capital to earn a reasonable rate of return.

This relatively unknown tax-free solution has been quietly used by America’s wealthiest families to cut taxes and preserve capital.

The Tax-Free Pension Alternative, also known as living benefit life insurance or a Tax-Free IUL eliminates taxes and stock market losses. It has been called a perfect retirement solution.

You don’t lose money when the markets go down, so you are never digging out of an investment hole!

You Share in Market Upside when Markets go up, up to a cap rate currently 13.0% to 16.0%!

You’ll Earn Reasonable Rates of Return!

Your Gains are locked in annually, so you never give back profits already earned!

Tax-Free Penalty Free Withdrawals at any age, the ultimate tax shelter!

You can generate a Tax-Free Income You Won’t Outlive!

New Retirement Planning Ideas can mitigate retirement tax-traps on previous contributions and eliminate them on new contributions.

Retirement plans such as IRAs, 401(k)s and 403(b)s are heavily taxed when you withdraw money. This looming tax-trap is a ticking time bomb that could blow up your retirement dreams. Your looming tax-trap could be 6 figures. The tax-free pension alternative gets rid of taxes on future contributions once and for all. Additional strategies can help limit the damage on past contributions.

Many people by default follow conventional wisdom. The same path their parents and grandparents followed. They max contribute to a 401(k) or 403(b) retirement plan and in doing so they subject their future retirement withdrawals to substantial income taxes and stock market losses. The double whammy of taxes and stock market losses could crush your retirement dreams.

Tax-Free is better. Watch the short video, read the eBook referenced in the video and call us with comments and questions.

You might have heard of IULs and wondered how they worked, and if they were right for you! Some of you might have thought they were too good to be true, that there must be a catch. There is no catch, there are some tradeoffs that most informed people are happy to live with.

There is a little known IRS strategy that the wealthiest top 10% of American Families, including the top 1% have been using for more than 20 years to cut taxes and preserve capital. The Strategy works. The Tax-Free IUL can produce a Tax-Free Income You Won’t Outlive! The strategy has also been known to double, even triple after tax income compared to a 401(k) or 403(b) retirement plan.

This retirement strategy, the tax-free pension alternative,is also known as living benefit life insurance and the tax-free IUL.

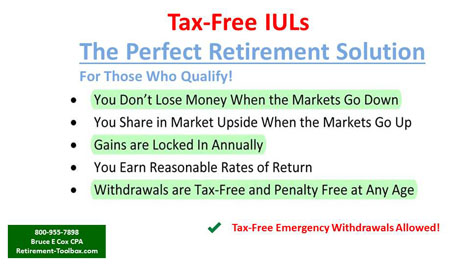

Tax-Free IULs are an IRS strategy with no downside risk. It has been called the perfect retirement solution.

• You don’t lose money when the markets go down!

• Share in Market Upside when Markets go up!

• Earn Reasonable Rates of Return!

• Gains Locked In Annually!

• Tax-Free Penalty Free Withdrawals at any age!

• Tax-Free Income You Won’t Outlive!

You have seen the stories, a staggering number of Professional Athletes and Entertainers filing Bankruptcy despite earning millions of dollars in salary or royalties. 78% of NFL players, 60% of NBA players and a large number of MLB players are bankrupt within 5 years of leaving the game. Plenty of Celebrities and Entertainers, actors, musicians, singers have joined the list too.

You can secure your financial future with a little known tax-free solution that America’s wealthiest families use to preserve capital and cut taxes.

Imagine retiring at age 35 with $301,000 of tax-free income for life; or at age 40 with $384,000 of tax-free income for life. It’s possible to make this happen with a little discipline. Beginning at age 25 you invest $500,000 per year for 5 years and average 7% per year on your money. Historical returns have averaged over 8%.

The Tax-Free Pension Alternative, An Under the radar strategy for Athletes, Entertainers and other High Earners. Strategy can Secure your financial future.

This little known strategy has flown under the radar for 20 years. Most advisors have never heard about the strategy or did not realize how powerful it has become.

It has been called The Perfect Retirement Solution and The 401(k) Replacement. It is a tax-free pension alternative and is also known as living benefit life insurance or the Tax-Free IUL. This tax-free solution works.

• You don’t lose money when the markets go down, so you are never digging out of an investment hole!

• You Share in Market Upside when Markets go up, up to a cap rate currently 13.5% to 16.0%!

• You’ll Earn Reasonable Rates of Return!

• Your Gains are locked in annually, so you never give back profits already earned!

• Tax-Free Penalty Free Withdrawals at any age, the ultimate tax shelter!

• You can generate a Tax-Free Income You Won’t Outlive!

During the Financial Market Melt Down, none of our clients lost money in their tax-free pension alternative. Their money was safe and secure. The same tax-free solution can work for you.

• So, if you hate paying taxes and hate even more losing money in the stock market, pay close attention.

• If you are worried you won’t have enough money to enjoy your retirement, this strategy will help you generate a tax-free income you won’t outlive.

• If you want to implement a gifting strategy for your children or grandchildren, the tax- free IUL is a vehicle that can keep on giving with a lifetime of tax-free income.

• If you like the idea of having a tax-free emergency fund to tap as needed, the tax-free retirement plan is for you.

• If you would like to be your own bank, funding big ticket items with retirement funds, paying interest to yourself rather than a bank, this could work for you.

Fortunately, the tax-free retirement solution addresses all of the above.

Tired of Losing Money in the Stock Market? You can Get Rid of Stock Market Losses and Taxes on Your Retirement Income Once and For All!

2008 Financial Market Melt DownYo-Yo Volatility and Gut Wrenching Stock Market Losses are eliminated with a Tax-Free Pension Alternative or Tax-Free IUL

Simply do what the Wealthiest American Families do to avoid taxes and not lose money in the stock market. They use a little known IRS approved strategy that has been called the perfect retirement solution for those who qualify. This tax-free pension alternative is also known as living benefit life insurance or the tax-free IUL.

• You don’t lose money when the markets go down, so you are never digging out of an investment hole!

• You Share in Market Upside when Markets go up, up to a cap rate currently 13.5% to 16.0%!

• You’ll Earn Reasonable Rates of Return!

• Your Gains are locked in annually, so you never give back profits already earned!

• Tax-Free Penalty Free Withdrawals at any age, the ultimate tax shelter!

• You can generate a Tax-Free Income You Won’t Outlive!

Free download and more videos https://www.bruceecoxcpa.com/

• So, if you hate paying taxes and hate even more losing money in the stock market, pay close attention.

• If you are worried you won’t have enough money to enjoy your retirement, this strategy will help you generate a tax-free income you won’t outlive.

• If you are rolling over money in CDs because you fear stock market losses, with this tax- free retirement strategy, you don’t lose money when the markets go down.

• If you have not put enough money away for retirement and need a catch up solution, this strategy could work for you.

• When you recognize the tax-free retirement plan can generate 3 to 4 times more income after taxes than a 401(k) or 403(b) retirement plan, you’ll want to replace your retirement plan with the tax-free retirement plan.

• If you want to implement a gifting strategy for your children or grandchildren, the tax- free IUL is a vehicle that can keep on giving with a lifetime of tax-free income.

• If you like the idea of having a tax-free emergency fund to tap as needed, the tax-free retirement plan is for you.

• If you would like to be your own bank, funding big ticket items with retirement funds, paying interest to yourself rather than a bank, this could work for you.

Fortunately, the tax-free retirement solution addresses all of the above.

New eBook tells how to get rid of stock market losses once and for all. You’ll keep more of your money with a tax-free retirement plan, plus you could generate 3 times more after tax retirement income compared to your 401(k) plan. Use the secret America’s wealthiest Families use to avoid taxes and not lose money in the stock market. The Strategy works. During the Financial Market melt down of 2008, none of our clients lost money in their tax-free retirement plan due to market volatility. Their Money was safe and secure and their income was steady and reliable.

This little known IRS approved strategy has largely flown under the radar for the last 20 years. Most Advisors never heard about it, or did not realize how powerful the strategy had become.

You have just been exposed to the strategy that can get of stock market losses and taxes on your retirement income once and for all. Learn more about this tax-free pension alternative, also known as living benefit life insurance.

Lawyers Accountants Keep More of Your Money with a Tax-Free Retirement Plan

It’s what you keep after taxes that counts. IRS allowed strategy can triple your retirement income after taxes compared to heavily taxed retirement income taken from your 401(k) or 403(b) retirement plan.

Conventional wisdom is to max fund your 401(k). This could costs you hundreds of thousands of dollars in taxes and market losses. Tax-Free Pension Alternative is the better choice.

Lawyers and Accountants you can keep more of your money with a Tax-Free Retirement Plan and generate 3 times more after tax income compared to your 401(k). Use the secret of the top 10% of America’s Wealthiest Families. They use the secret IRS approved strategy to avoid taxes and not lose money in the stock market. This little known strategy has flown under the radar for 20 years. Most advisors have never heard about the strategy or did not realize how powerful it has become.

Lawyers and Accountants keep more of your money with a tax-free retirement plan.

This tax-free pension alternative has been called The Perfect Retirement Solution and The 401(k) Replacement.

• You don’t lose money when the markets go down, so you are never digging out of an investment hole!

• You Share in Market Upside when Markets go up, up to a cap rate currently 13.5% to 16.0%!

• You’ll Earn Reasonable Rates of Return!

• Your Gains are locked in annually, so you never give back profits already earned!

• Tax-Free Penalty Free Withdrawals at any age, the ultimate tax shelter!

• You can generate a Tax-Free Income You Won’t Outlive!

Medical Professionals, Triple Your Retirement Income After Taxes and Retire Early

It’s what you keep after taxes that counts. IRS allowed strategy can triple your retirement income after taxes compared to heavily taxed retirement income taken from your 401(k) or 403(b) retirement plan.

Would You Retire Early If You Had 3x more spendable cash during retirement than you anticipated from your IRA, 401(k) or 403(b) plan?

Obamacare is squeezing Physicians Incomes adding to Physicians stress levels.

Medical Professionals, are Government Regulations and Taxes getting to you? How about retiring early with 3 times the after-tax income vs. your 401(k) or 403(b) retirement plan?

Simply use the secret of the top 10% of America’s wealthiest families. It has been known to double, even triple after-retirement income vs. 401(k)s and 403(b) retirement plan.

Imagine going from $25,000 per year in after-tax retirement income to $75,000 in tax-free retirement income, or $100,000 to $300,000.

The strategy works and it could work for you. The Wealthiest American families use it to avoid taxes and to get rid of stock market losses once and for all. This little known IRS allowed strategy that has been called the perfect retirement solution for those who qualify. The Tax-Free Pension Alternative is also known as living benefit life insurance. You or a family member must be insurable to qualify.

• You don’t lose money when the markets go down, so you are never digging out of an investment hole!

• You Share in Market Upside when Markets go up, up to a cap rate currently 13.5% to 16.0%!

• You’ll Earn Reasonable Rates of Return!

• Your Gains are locked in annually, so you never give back profits already earned!

• Tax-Free Penalty Free Withdrawals at any age, the ultimate tax shelter!

• You can generate a Tax-Free Income You Won’t Outlive!

Kindle version $2.99

• So, if you hate paying taxes and hate even more losing money in the stock market, pay close attention.

• If you are worried you won’t have enough money to enjoy your retirement, this strategy will help you generate a tax-free income you won’t outlive.

• If you are rolling over money in CDs because you fear stock market losses, with this tax- free retirement strategy, you don’t lose money when the markets go down.

• If you have not put enough money away for retirement and need a catch up strategy, this strategy could work for you.

• When you recognize the tax-free retirement plan can generate 3 to 4 times more income after taxes than a 401(k) or 403(b) retirement plan, you’ll want to replace your retirement plan with the tax-free retirement plan.

• If you want to implement a gifting strategy for your children or grandchildren, the tax- free IUL is a vehicle that can keep on giving with a lifetime of tax-free income.

• If you like the idea of having a tax-free emergency fund to tap as needed, the tax-free retirement plan is for you.

• If you would like to be your own bank, funding big ticket items with retirement funds, paying interest to yourself rather than a bank, this could work for you.

Fortunately, the tax-free retirement solution addresses all of the above.