Retirement-Toolbox.com

Tax-Free Retirement Income, High Yield CD Alternatives and other Safe Income Strategies

Retirement-Toolbox.com

Find us on Google+Tweet |

800-955-7898Bruce E. Cox CPABruceECoxCPA.com |

Retirement Strategies: The Tax-Free Pension Alternative

Tax-Free IL eBook published on Amazon.com

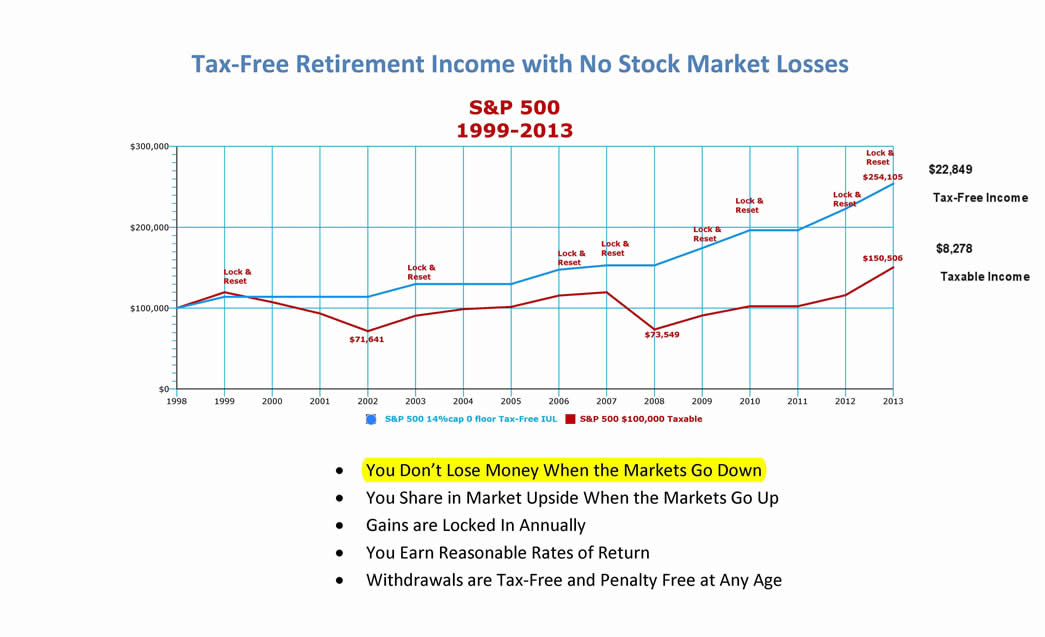

Imagine Getting Rid of Stock Market Losses and Still Earning A Reasonable ROR

403(b) or IRA-3.jpg)

There is a better strategy. It is safe and it works. I can show you a little-known IRS approved strategy ... you can use right

now to insulate your retirement from the looming tax traps that lie ahead.

This IRS approved Tax-Free Retirement Plan is better than an IRA, 401(k) or 403(b) retirement plan.

Call 800-955-7898 to get started!

Tax-Free Wealth Building ... The Best Kept Secret to Financial Independence and Retirement Security

Tax-Free Retirement Plans

How to Jump-Start a Tax-Free Retirement PlanRetirement Plan Tax Traps - Robbing you in plain sight and you probably don’t know it.

Wake up! Did you know that every time you withdraw $1,000 from a traditional IRA, 401(k) or 403(b) retirement plan The Government grabs about $400? Leaving you with only $600 after federal and state income taxes.

That’s right, 40% of every withdrawal goes to the government. It could be more, could be less.

You can stop this nonsense with a tax-free retirement plan.

Plan in the event of an untimely death, protecting and providing for your loved ones. ______________________________________________________

“There are two systems of taxation in our country: one for the informed and one for the uninformed.” The often quoted Honorable Learned Hand U.S. Appeals Court Justice ___________________________________________________________ Act now. Benefit from a million dollar idea from the Retirement-Toolbox.

You’ll need a retirement check to replace a pay check when you retire and these checks might have to last you 25 to 30 years. You cannot count on an inheritance or winning the lottery. You prepare for the future. So you are saving money on a systematic basis, regularly contributing to an IRA or 401(k) and falling into the tax trap.But they said it would save me taxes. They are wrong. It only defers taxes. The tax bite on withdrawals is much harsher.Example, you save $500/month, $6,000/year for 30 years.Total contributions $180,000.Tax savings (deferral) $45,000 (25% tax bracket)Tax savings (deferral) $60,000 (33% tax bracket)That is $1,500 to $2,000 per year in tax deferrals.__________________________________________________30 years later account value $600,000 (6.89% average return)30 years later account value $800,000 (8.31% average return)__________________________________________________Taxes due on withdrawals $240,000 to $320,000.Governments take 40%.But won’t I be in a lower tax bracket?You will probably lose your biggest tax deduction, mortgage interest. Most people have the goal of paying off their home mortgage. Children are grown, so dependent deductions are gone too.If Barack Obama is reelected, do you think your tax rates will go up?_____________________________________________________So, are you better off paying taxes on the seed or on the harvest?Fund the $180,000 with after tax dollars and owe no taxes on the growth or use pre-tax dollars and owe lots of taxes on the growth.Defer $1,500 to $2,000 a year in taxes but owe $240,000 to $320,000 on the withdrawals.Or skip the annual deferral and owe no taxes on the withdrawals.Shouldn’t you be informed and save the right way, with a tax-free retirement plan? Don’t fall into the tax trap and lose 40% or more of your retirement check to taxes. The wrong choices get the wrong results.Unleash the power of tax-free growth and the magic of compounding. It is your money. Keep the full $1,000. Switch to a Tax-Free Retirement Plan. It's a no Brainer. Call 800-955-7898 for more information.This is a million dollar idea! It could add millions to your family's life time income.Bruce E Cox CPA Retirement-Toolbox LLC 240 Regina Street Philadelphia PA 19116 267-731-6706800-955-7898

P.S. If you don’t mind forking over 40% of your retirement savings to pay for more reckless government spending, then keep doing what you have been doing.

Politicians count on uninformed taxpayers to pay for their bridges to nowhere, their earmarks, failed stimulus, Solyndra and taxpayer bailouts.

Be smart. Let the uninformed pay. You don’t have a Patriotic duty to pay more taxes than the law requires. “Anyone may arrange his affairs so that his taxes shall be as low as possible; he is not bound to choose that pattern which best pays the treasury. There is not even a patriotic duty to increase one’s taxes. Over and over again the Courts have said that there is nothing sinister in so arranging affairs as to keep taxes as low as possible. Everyone does it, rich and poor alike and all do right, for nobody owes any public duty to pay more than the law demands: Taxes are enforced exactions, not voluntary contributions. To demand more in the name of morals is mere cant.”–Honorable Learned Hand, U.S. Appeals Court Judge, Helvering v. Gregory, 69 F.2d 809 (1934)* During the Financial Market Melt Down of 2008 the Nasdaq and S&P 500 were down 40%. Many people saw their IRAs, 401(k)s stocks and mutual funds cut in half, putting them in a position of needing to double their remaining funds just to get even. At 6% that will take 12 years.

Imagine saving and sacrificing for 20 to 30 years only to have your savings cut in half when you need to tap the funds.

None of our clients investing in the tax-free retirement plan lost money due to market volatility. Their money was safe and secure. Their income was steady and reliable.

They eliminated market losses and shared in market upsides earning reasonable rates of return.

|

||||

---------------------------------------------------------------------------------- Profit from my 35+ years experience working with high net worth individuals, families, entrepreneurs and businesses, helping them create wealth, keep their wealth and pass it on to the next generation. You can benefit too.A CPA, I have been a stockbroker with Series 7, 24 & 27 licenses, an insurance producer, the Chief Financial Officer of a private equity group (Venture Capital) that raised private equity funds and then took a company public, a mortgage broker and owner of a mortgage company. Safe Income Strategies work, and you don't have to be super rich for them to work for you.----------------------------------------------------------------- |

||||

![]()

Bruce

E. Cox CPA • 240 Regina Street• Philadelphia PA 19116 |

Copyright © 2014- 2012

Bruce E. Cox, CPA. All rights reserved

|